Cost Segregation

Boost Your Bottom-Line

Cost segregation studies can lower your current-year tax liability and free up more capital.

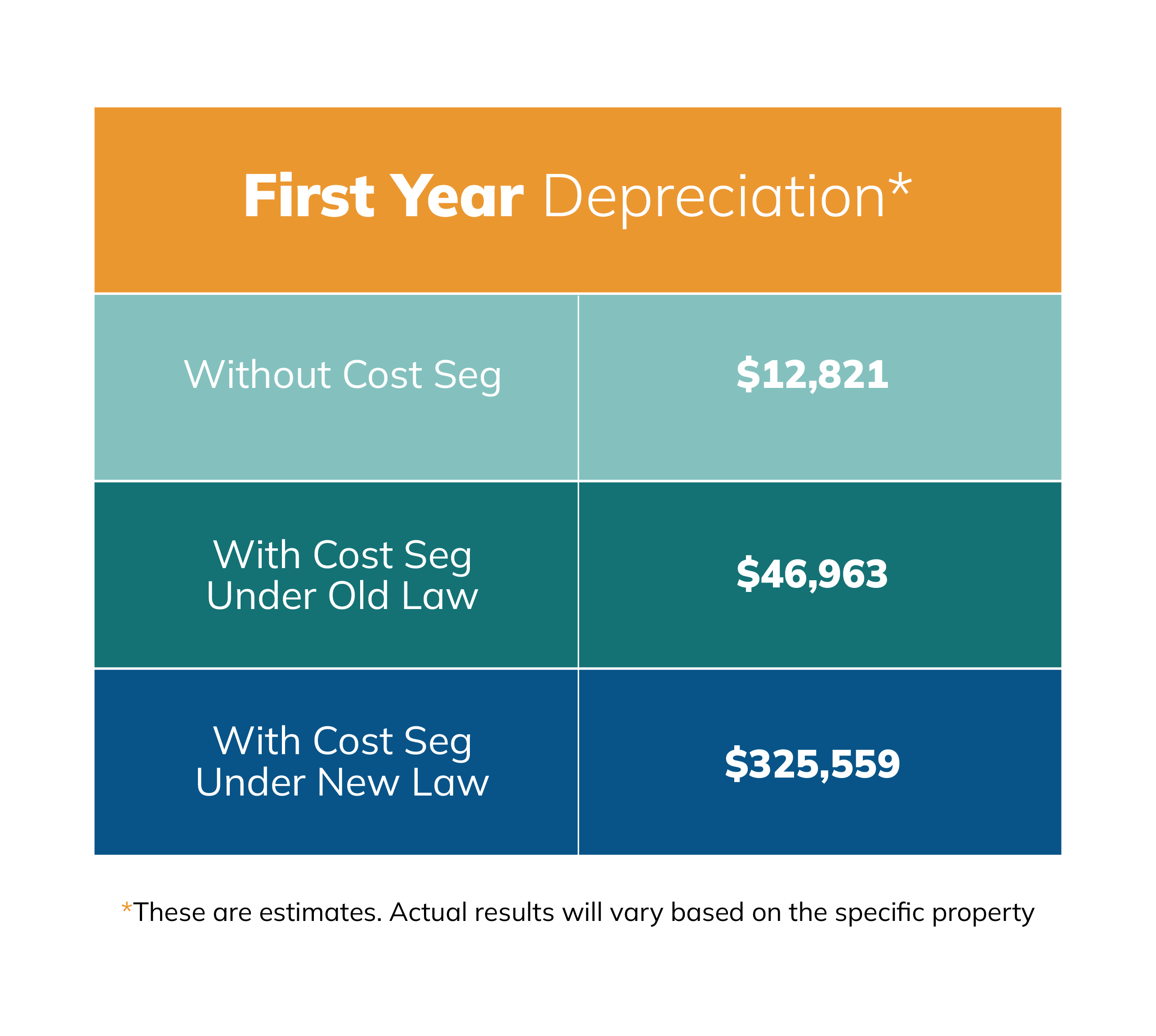

Making an investment in your organization by purchasing, constructing or upgrading property, can be a valuable tax strategy. A cost segregation study separates real property into various depreciable categories, and allows taxpayers to depreciate property over much shorter periods of time than the typical 39-year (or 27.5-year) period. By taking deductions sooner, you lower your current-year tax liability and free up more capital.

The Benefits of a Cost Segregation Study Include

An average return on investment of 54:1

Substantial accelerated tax deductions

Increased cash flow

Special depreciation allowances (i.e., Section 179 or bonus depreciation)

Our work is performed in accordance with current tax authority, including the Internal Revenue Code, court decisions, revenue procedures, revenue rulings and Treasury regulations. Our cost segregation specialists apply the standards in the “Cost Segregation Audit Techniques Guide” used by the IRS. Our Certified Cost Segregation Specialists have the highest level of accreditation in the industry, and we’re one of only 16 firms in the country to employ such experts.

Who should consider a cost segregation study?

A taxpayer could reduce taxes and greatly increase cash flow through a study if:

The company is planning to or has recently constructed or purchased a building

The company recently renovated an existing building it owns or leases

The construction/purchase/renovation price was at least $300,000

Type of Properties That Qualify

Office buildings

Retail centers

Banks

Apartment buildings

Manufacturing facilities (heavy or light)

Restaurants

Hotels/motels

Grocery stores

Auto dealerships

Theaters

Golf courses

Research and development centers

Cost Segregation

Our team of experts is dedicated to helping you unlock the hidden value in your properties and achieve your financial goals.

Cost Segregation

We can accelerate depreciation deductions, resulting in substantial tax savings.

Related Services

Streamlining Tax Strategies for Business Success

There are federal and state tax credits, plus additional rebates and incentives that can be stacked to save businesses money on green energy equipment.