Navigating OBBBA Payroll & Reporting Changes Before 2026

The One Big Beautiful Bill Act (OBBBA) is ushering in major payroll and information reporting changes that every employer should be preparing for now. Beginning in 2026, businesses will face higher reporting thresholds, new payroll codes, and additional tracking requirements for employee tip and overtime income. These updates are designed to simplify reporting on paper, but in practice, they may add new layers of compliance complexity for employers and payroll providers.

Increased Reporting Thresholds Go into Effect in 2026

Businesses generally must report payments made during the year that equal or exceed the reporting threshold for rents, salaries, wages, premiums, annuities, compensation, remuneration, emoluments, and other fixed or determinable gains, profits and income. Similarly, recipients of business services generally must report payments they made during the year for services rendered that equal or exceed the statutory threshold. This information is reported on information returns, including Forms W-2, Forms 1099-MISC and Forms 1099-NEC.

Currently, the reporting threshold amount is $600 for Forms 1099-MISC and Forms 1099-NEC. For payments made after 2025, the OBBBA increases the threshold to $2,000, with inflation adjustments for payments made after 2026. There is no minimum income threshold that triggers W-2 reporting. Employers must issue a W-2 to each employee who received wages, regardless of the amount. This is true for 2025 and beyond. The OBBBA didn’t make any changes to this.

Reporting Qualified Tip Income and Qualified Overtime Income

Effective for 2025 through 2028, the OBBBA establishes new deductions for employees who receive qualified tip income and qualified overtime income. Because these are deductions as opposed to income exclusions, federal payroll taxes still apply to this income. So do federal income tax withholding rules. Also, tip income and overtime income may still be fully taxable for state and local income tax purposes.

The issue for employers and payroll management companies is reporting qualified tip and overtime income amounts so that eligible workers can claim their rightful federal income tax deductions. In August, the IRS announced that for 2025 there will be no OBBBA-related changes to federal information returns for individuals, federal payroll tax returns or federal income tax withholding tables. The 2025 versions of Form W-2, Forms 1099, Form 941, and other payroll-related forms and returns will be unchanged.

Nevertheless, employers and payroll management companies should begin tracking qualified tip and overtime income immediately and implement procedures to retroactively track qualified tip and overtime income amounts that were paid going back to January 1, 2025. The IRS will provide transition relief for 2025 to ease compliance burdens.

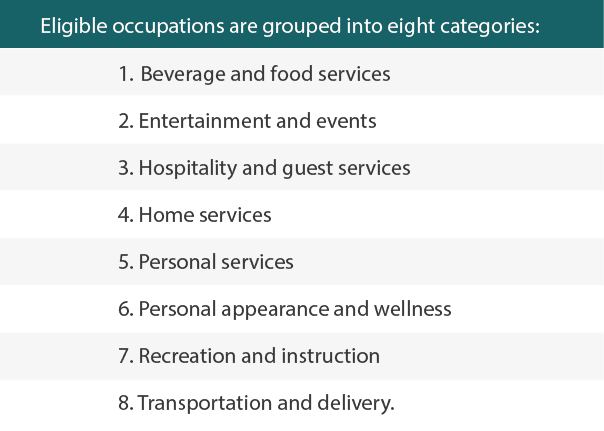

Proposed Regulations List Tip-Receiving Occupations

In September, the IRS released proposed regs that include a list of tip-receiving occupations eligible for the OBBBA deduction for qualified tip income.

The IRS added three-digit codes to each eligible occupation for information return purposes.

2026 Form W-2 Draft Version

The IRS has released a draft version of the 2026 Form W-2. It includes changes that support new employer reporting requirements for the employee deductions for qualified tip income and qualified overtime income and for employer contributions to Trump Accounts, which will become available in 2026 under the OBBBA.

Specifically, Box 12 of the draft version adds:

Code TA to report employer contributions to Trump Accounts,

Code TP to report the total amount of an employee’s qualified cash tip income, and

Code TT to report the total amount of an employee’s qualified overtime income.

Box 14b has been added to allow employers to report the occupation of employees who receive qualified tip income.

Leverage CSH for Trusted Tax Expertise

With so many payroll and reporting updates on the horizon, businesses can’t afford to take a “wait and see” approach. CSH’s Tax Advisors and Payroll Compliance professionals help employers interpret evolving OBBBA requirements, implement proactive tracking systems, and stay ahead of IRS updates. Our team partners with you to ensure accurate reporting, minimize compliance risk, and position your business for a seamless transition into 2026 and beyond.