It’s no secret that the trend of active community bank mergers is continuing. With almost 290 transactions in 2015, approximately 300 in 2014 and almost 250 in 2013, bank M&A activity is likely to continue for the foreseeable future. In fact, in January of this year several high profile banking analysts stated that M&A transactions could spike in 2016, including Rafferty Capital financial analyst Richard Bove who believed 2016 could be one of the most significant years for bank mergers in the past decade. With approximately 130 bank mergers in the first six months of 2016, we’re likely not going to reach the 400 transaction level that some analysts had predicted, but bank M&A continues to be a formidable force in the industry.

Conditions are ripe for consolidation

The primary drivers of today’s bank M&A environment are a perfect storm of:

1. Weak profits due to a challenging interest rate environment and continued sluggish loan growth.

2. Increased expenses required to comply with an increased regulatory burden, and capital expenditures on technology necessary to stay competitive and keep systems and information secure.

This storm of rising costs and lower margins is having a major impact on growth opportunities. When executive boards and leadership teams review their options for growth, many see M&A as the most attractive and realistic option. Consolidation can provide the financial, operational and personnel scale smaller banks need to meet market, regulatory and shareholder expectations. Banks are able to grow larger, which allows them to distribute added costs for compliance and technology while remaining profitable even as margins are thin.

As survival concerns ease, a focus on growth

Most banks are not considering M&A activity because they are weak or are struggling to survive, but rather because they are struggling to grow. After the recent financial crisis, M&A was used as a last resort for banks that were sinking or didn’t have strong leadership to take over. But now we’re seeing M&A among healthy banks to help move the needle on their growth prospects.

Regional banks finally return to M&A

Having been sidelined from the M&A game since the financial crisis, several regional banks reentered the M&A arena recently, including BB&T, Key Bank and Huntington Bank. BB&T closed on two acquisitions in 2015, including Bank of Kentucky ($1.9 billion in assets) and Susquehanna Bancshares ($18.7 billion in assets). Immediately upon closing the Susquehanna transaction, BB&T announced a $1.8 billion acquisition of National Penn Bancshares, which would provide another $9.6 billion in assets.

Key Bank’s acquisition of First Niagara Financial Group would increase Key’s size by 40% and add $39 billion in assets, making the merged bank the 13th largest bank in the nation. In January of this year, Huntington Bank announced its acquisition of FirstMerit, which would give Huntington more than $25 billion in new assets.

It will be interesting to see whether more large regional banks enter the M&A game later this year. While there were several acquisitions recently, ultimately, bank consolidation will continue to be concentrated at the community bank level – at least based on the total number of transactions.

A new reality or more of the same?

Bank consolidation is nothing new. In fact, the total number of banks and savings institutions has decreased from roughly 15,000 in 1990 to less than 6,500 today. The causes of consolidation at various times during this period have varied – from failures during times of crisis, to the relaxation of state branching and national interstate banking restrictions, and voluntary mergers between unaffiliated community banks.

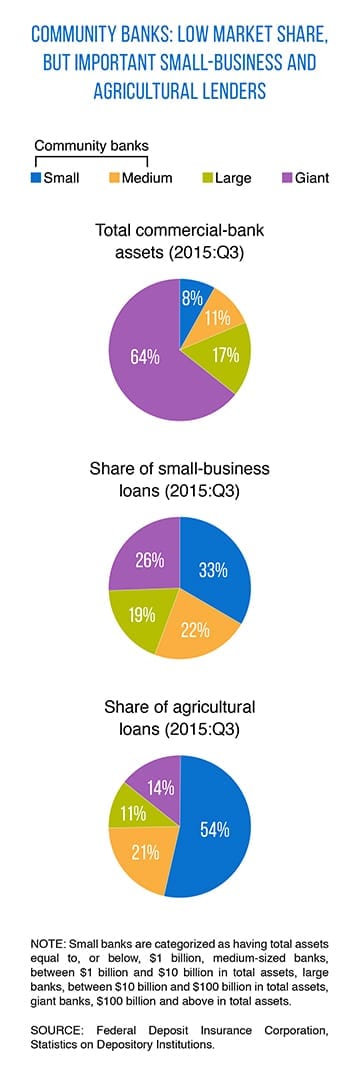

Despite their decreasing numbers, community banks continue to play a unique and vital role in the U.S. economy. While their share of total bank assets is low, they provide a disproportionate share of small business and agricultural lending (see chart at right). Still, many community banks consider M&A their best option to achieve growth in the current banking environment.

An M&A transaction is a large undertaking, for both the buyer and seller. Clark Schaefer Hackett advisors can guide you through the process and help your institution take advantage of potential opportunities, overcome obstacles and navigate the complexities of consolidation.

For more information contact Scott Deters at [email protected].